Biden Tax Plan, Tax Rates Movin’ On Up

Ok, despite having three extra months, how many of you were last minute scrambling (like me) to pull everything together to file your taxes on time last week?

To celebrate, that tax-day (July 15th) is behind us and opening day is nearly here, we decided to have an initial look at potential winners and losers if former vice president Joe Biden’s corporate tax proposals were to become the law of the land. We focus on the three main corporate provisions of the Biden tax plan (based on the limited information available): (1) increase the U.S. statutory corporate tax rate from 21% to 28%, (2) double the Global Intangible Low-Taxed Income (GILTI) tax rate from 10.5% to 21% and (3) impose a 15% minimum tax on book income.

Time for the Tax Rate Estimator

If there’s a chance that tax rates might be changing we suggest you try our handy dandy Tax Rate Estimator (which was quite popular in the midst of tax reform and more recently has been used to help investors get at sustainable tax rates for the companies they own/follow). The Estimator was first released on Halloween 2017 and has since gone through a few iterations. But the underlying framework remains the same, it builds an estimate of GAAP effective tax rates from the ground up. For further background check out Game of Tax Reform #7, Beyond the Wall – New Tax Rates, But Are They Sustainable?.

If there’s a chance that tax rates might be changing we suggest you try our handy dandy Tax Rate Estimator (which was quite popular in the midst of tax reform and more recently has been used to help investors get at sustainable tax rates for the companies they own/follow). The Estimator was first released on Halloween 2017 and has since gone through a few iterations. But the underlying framework remains the same, it builds an estimate of GAAP effective tax rates from the ground up. For further background check out Game of Tax Reform #7, Beyond the Wall – New Tax Rates, But Are They Sustainable?.

Lots of Potential Tax Rate Losers

Focusing on the companies in the S&P 500 (ex-real estate and companies domiciled outside the U.S.), we started with their most recent fiscal year-end tax info (a key simplifying assumption). Then we back of the envelope estimate the impact on effective tax rates of two provisions in the Biden plan: increasing the statutory tax rate to 28% and doubling the GILTI rate to 21% (we analyze the effect of the 15% minimum tax separately below and for now chose to ignore other aspects of the plan).

Please keep in mind that this is our first cut at estimating the impact of the Biden plan and expect to update and fine tune the analysis over time (especially as more details are made available). In addition, our estimates are a starting point, we’re not trying to predict the exact tax rate a company will report (we’d need a crystal ball for that). Instead, our goal is to help you estimate the tax rate you’d put in your model going forward if the Biden tax plan were to happen.

Please keep in mind that this is our first cut at estimating the impact of the Biden plan and expect to update and fine tune the analysis over time (especially as more details are made available). In addition, our estimates are a starting point, we’re not trying to predict the exact tax rate a company will report (we’d need a crystal ball for that). Instead, our goal is to help you estimate the tax rate you’d put in your model going forward if the Biden tax plan were to happen.

We estimate that under the Biden plan, effective tax rates for a subset of S&P 500 companies would increase by almost 800 bps on average, from 18.7% in 2019 to 26.7%, resulting in a nearly 10% hit to earnings. As you can see in Exhibit 1, earnings for certain sectors (those with lower tax rates today) would get hit harder than others.

We estimate that under the Biden plan, effective tax rates for a subset of S&P 500 companies would increase by almost 800 bps on average, from 18.7% in 2019 to 26.7%, resulting in a nearly 10% hit to earnings. As you can see in Exhibit 1, earnings for certain sectors (those with lower tax rates today) would get hit harder than others.

.PNG)

Don’t forget there’d also be an impact on the balance sheet, a higher tax rate could result in an increase to both deferred tax liabilities and deferred tax assets (see our August 24, 2017 piece, Making Game of Tax Reform: How to Estimate the Impact of a Tax Rate Cut on Deferred Tax Assets).

Some Companies Hit Harder than Others

At the company level, we estimate that tax rates would increase for 96% of those analyzed (there’s a few strange anomalies where tax rates drop, mostly due to one-off items), including 109 companies that are tax rate losers where tax rates could jump by 1,000 bps or more. There are some (relative) tax rate winners, like the 33 companies where tax rates increase by less than 250 bps.

At the company level, we estimate that tax rates would increase for 96% of those analyzed (there’s a few strange anomalies where tax rates drop, mostly due to one-off items), including 109 companies that are tax rate losers where tax rates could jump by 1,000 bps or more. There are some (relative) tax rate winners, like the 33 companies where tax rates increase by less than 250 bps.

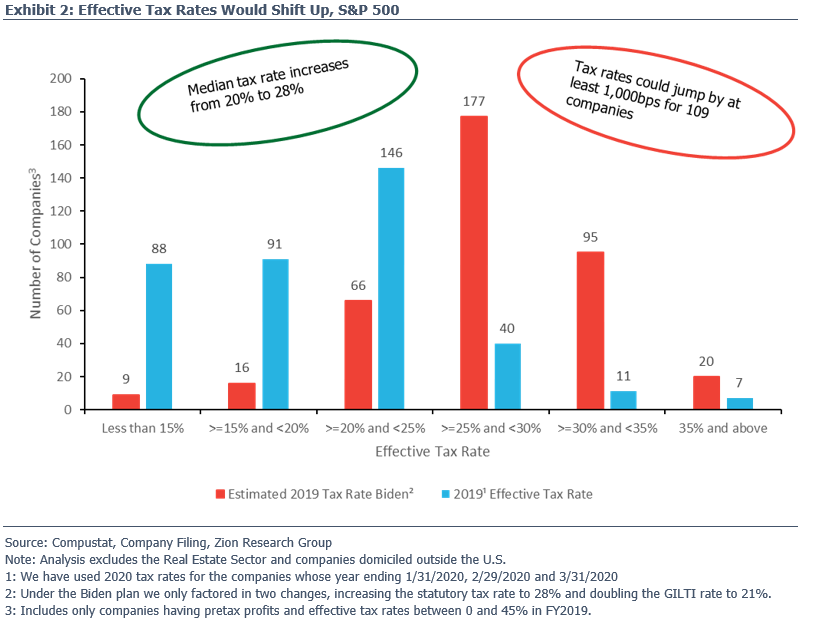

As you can see in Exhibit 2, we estimate that most effective tax rates under the Biden plan would fall somewhere in between 20% and 35%, with a median tax rate of 28%, up from 20% in 2019.

When we drill down to the impact on the bottom line, we estimate that the median hit to earnings is 9.7%, and for 87 companies, earnings could fall by more than 10%. Looking on the brighter side, there are 35 companies where earnings could get hit by less than 5%.

15% Minimum Tax on Book Income, $37 Billion Hit for S&P 500

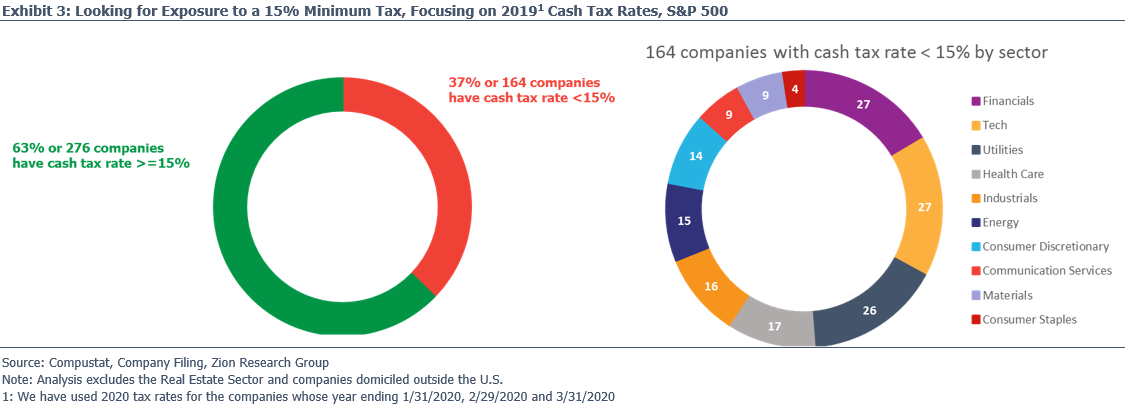

The Biden plan would also slap a 15% minimum tax on book income for those companies with over $100 million in profits. We’re going to assume, as other studies have, that it would be set up as an alternative minimum tax (i.e., calculate the tax a company owes based on the tax code, compare it to 15% of total book income and pay whichever is higher). That means the 164 companies in the S&P 500 with cash tax rates less than 15% are potentially most at risk.

Minimum Tax is Highly Concentrated, Five Companies Account for Nearly Half

To give you a rough idea of the potential impact, we’re going to pretend that the 15% minimum tax was in effect for 2019. We’d expect the actual impact to be less than our estimates as you’d most likely be starting from a point where companies are paying higher taxes (due to the proposals discussed above). In addition, companies might be allowed to use NOLs to reduce this tax bill, which we have not factored into our analysis.

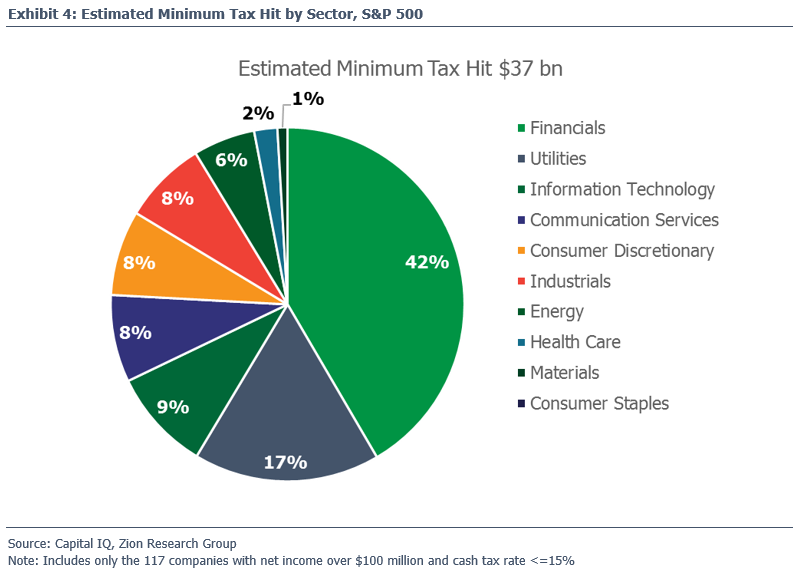

There are 117 companies in the S&P 500 with over $100 million in net income that had a cash tax rate of less than 15% in 2019. Those companies generated $401 billion of total book pretax income during 2019. Apply a 15% tax rate and you get a minimum tax of $60 billion as compared to the $23 billion of taxes they actually paid in 2019. In other words, we estimate these companies would owe an additional $37 billion in taxes to Uncle Sam.

Taking a look at that tax burden by sector in Exhibit 4, you can see that two sectors, Financials and Utilities (remember, Utilities may share some of that tax burden with their customers), would be responsible for almost 60% of the estimated minimum tax hit for the S&P 500.

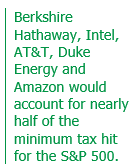

We estimate there are 16 companies that would owe more than $500 million of additional tax as a result of the minimum tax, accounting for nearly 70% of the total due by the S&P 500. At the top of that list are Berkshire Hathaway, Intel, AT&T, Duke Energy and Amazon, which would be responsible for nearly half of the additional tax due.

We estimate there are 16 companies that would owe more than $500 million of additional tax as a result of the minimum tax, accounting for nearly 70% of the total due by the S&P 500. At the top of that list are Berkshire Hathaway, Intel, AT&T, Duke Energy and Amazon, which would be responsible for nearly half of the additional tax due.

You might be wondering why not compare the estimated minimum tax to the taxes that the company paid in the U.S., isn’t the difference between those amounts the additional tax that the company would owe? It is, but the Biden plan apparently applies to global book income and it allows companies to use foreign tax credits to reduce the minimum tax due. Our methodology roughly captures that by using total taxes paid. Plus, companies don’t disclose U.S. taxes paid (would be nice if the FASB could finally help with that), though we could take a crack at estimating it if you’re interested.

Problems with a Tax on Book Income and Potential Changes in Behavior

Based on the limited info available about the 15% minimum tax, we could see a number of potential problems and changes in behavior; here are four to consider:

Non-GAAP on steroids! With a real economic incentive to keep book income down (paying less in taxes), we’d expect companies will go all in on non-GAAP, trying to paint an even prettier picture of their results (especially if they try to make their GAAP results look worse to pay less in taxes).

Non-GAAP on steroids! With a real economic incentive to keep book income down (paying less in taxes), we’d expect companies will go all in on non-GAAP, trying to paint an even prettier picture of their results (especially if they try to make their GAAP results look worse to pay less in taxes).

- The FASB would effectively be setting tax policy, who elected them to do that job? We’d expect projects like amortizing goodwill would suddenly get very popular. In fact, on July 15th (Tax Day), six of the seven board members were supportive of doing research on the possibility of amortizing goodwill (we can’t make this stuff up). The cost/benefit analysis of future accounting rule changes would be very different than today.

- Companies would set their own tax policy too, aren’t their lobbyists doing that now anyway? That’s a result of the wide variety of management judgment calls that go into GAAP earnings (e.g., shrink depreciable lives to increase depreciation expense to reduce earnings and pay less in taxes; or more write-offs?).

- Time to get packing. Increasing the tax rate would once again provide incentive for companies to leave the U.S. for the smiling shores of Ireland, etc. How about we actually try to fix the tax code instead?

Nine Other Reasons Why Tax Rates Could Head Higher from Here

Even if Joe Biden is not elected, there are a number of factors that could cause corporate tax rates to increase in the future (especially for multinationals), including:

- Someone eventually has to pay for all this stimulus spending (including you and me).

- BEAT (Base Erosion and Anti-Abuse Tax) tax rate increased from 5% to 10% last year (then 12.5% in 2026).

- Continued crackdown on base erosion and profit shifting outside the U.S. (despite Apple’s recent tax win over the European Commission) including more countries looking to tax the “digital economy” (e.g., France, Italy and the U.K have all implemented a digital tax).

- New NOL’s can only shield up to 80% of taxable income (though the CARES Act temporarily lifted the 80% cap on NOL usage for 2018 thru 2020, see our March 31, 2020 piece, Washington Attacks COVID-19 with CARES Stimulus – Top Ten List).

- Companies continue to pay the deemed repatriation tax through 2026 (remember it’s back-end loaded).

- In 2022, the limit on tax deductibility of interest expense switches from 30% of EBITDA to 30% of EBIT (the CARES Act temporarily raised the limit to 50% for 2019 and 2020).

- Also, in 2022, R&D will no longer be expensed immediately for tax but amortized over five years (domestic R&D) or 15 years (foreign R&D).

- Full expensing of capex will begin to phase out in 2023.

- A bit further down the road in 2026 both the GILTI (Global Intangible Low-Taxed Income) and FDII (Foreign Derived Intangible Income) tax rates increase from 10.5% to 13.125% and 13.125% to 16.4% respectively.

We’ve warned about increasing tax rates previously, for example, see our March 20, 2018 piece, Game of Tax Reform #7: Beyond the Wall – New Tax Rates, But Are They Sustainable?.

Kicking the tires on the companies you own/follow? We can help, from assisting with due diligence, to identifying risk, to helping with your models and more. For example, if you’re working on taxes, try out our Tax Rate Estimator.

Kicking the tires on the companies you own/follow? We can help, from assisting with due diligence, to identifying risk, to helping with your models and more. For example, if you’re working on taxes, try out our Tax Rate Estimator.

Take care,

Dave